Revenue recognition is the accounting process of recording income when cash is earned, not when received. This core revenue recognition principle makes sure that financial statements showcase the real performance of a business.

When it comes to SaaS, payments are often collected directly. In this scenario, the revenue recognition principle becomes important to avoid overstating revenue.

ASC 606 Revenue Recognition in SaaS

The ASC 606 revenue recognition standard gives SaaS companies a clear, structured way to handle revenue from client contracts. It works through a five-step model: identify the contract, define what you've promised to deliver (performance obligations), determine the price, allocate it appropriately, & finally recognize revenue only when those obligations are fulfilled.

For SaaS businesses, this usually indicates recognizing subscription revenue across the service period rather than doing it all on day one. Since SaaS products are delivered on an ongoing basis, revenue gets recorded uniformly over the subscription period. Thus, keeping your financials accurate and compliant.

Deferred Revenue Recognition in Subscription Models

Deferred revenue recognition is a key factor of SaaS accounting. When a client pays the amount in advance, it is considered as deferred revenue. This is because the service hasn't been delivered yet.

As each month passes and the service is rendered, a portion of that payment is counted as revenue. This approach aligns earnings with actual delivery and secures against financial errors that could mislead auditors or investors.

Role of Subscription Management Software in Compliance

Handling SaaS revenue recognition manually gets complicated fast due to plan upgrades, downgrades, usage-based billing, and mid-cycle contract changes. Subscription management software automates revenue schedules, tracks deferred balances, and ensures ongoing compliance with ASC 606 revenue recognition rules.

Beyond that, these platforms generate audit-ready reports and cut down on manual errors.

What Is Revenue Recognition?

Revenue recognition is the accounting process that determines when and how a business records its revenue, not when cash is received, but when the product/service is delivered to the customer. This is a foundational principle of accrual accounting, governed by two major standards: ASC 606 in the United States and IFRS 15 in international markets.

This matters more for SaaS businesses than it does in most industries. Customers often pay in advance for annual subscriptions, whereas companies deliver the service month by month. In other models, companies provide the service first and bill later based on usage. In both cases, revenue recognition ensures that income is recorded in the correct period, giving investors, auditors, and finance teams an accurate view of the company's financial performance.

The Revenue Recognition Principle

The revenue recognition principle is one of the foundational elements of accrual-basis accounting and US GAAP. It states that revenue must be recognized in the period in which it is earned when goods or services are delivered, regardless of when payment is received or when an invoice is issued.

Before ASC 606 unified the standards in 2014 (effective 2018 for public companies, 2019 for private companies), the revenue recognition principle was applied inconsistently across industries.

Each industry followed its own set of rules. Software companies operated under a separate regime (SOP 97-2), while professional service firms, telecom companies, and manufacturers each followed their guidance. This made revenue reporting inconsistent across companies, complicating analysis for analysts, investors, and regulators.[GR1.1]

ASC 606 replaced all of these with a single governing principle: "Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services." This principle forms the foundation of the five-step revenue recognition model covered in detail below.

Revenue Recognition Principle vs. Matching Principle

The revenue recognition principle works with the matching principle, [GR2.1]which means recording expenses in the same period as the revenue they help generate. Together, they ensure financial statements that reflect actual business performance, not just the timing of cash flows.

In SaaS, this is especially relevant. Companies often pay sales commissions and onboarding costs upfront but spread those costs across the customer subscription period under ASC 340-40. This helps match those costs with the revenue they generate.

For finance teams, the impact goes beyond accounting. It affects how revenue is reported to investors, how audits are conducted, and whether financial statements meet compliance requirements. Misapplying it [GR3.1]can mess up financial results and reduce trust in the numbers people rely on.

Why Revenue Recognition Matters in SaaS

SaaS businesses often collect subscription fees before the service is fully delivered. A user might pay monthly or annually, but the company earns that revenue month by month. Recording the full payment as revenue right away doesn’t just break accounting rules; it makes the early numbers look better than they really are, and the later ones look worse.

Revenue recognition in SaaS has direct implications across three key areas.

Regulatory Compliance and Legal Risk

Revenue recognition is governed by standards such as ASC 606 under US GAAP and IFRS 15 in global markets. For companies operating in India, Ind AS 115 applies as the local equivalent. Firms are required to follow them when preparing financial statements. Non-compliance can lead to regulatory action for public companies, forcing companies to revise their financial statements. It also damages trust with leaders and investors and creates tax issues when reports do not match the actual cash received.

Investor Trust and Fundraising Valuations

SaaS valuations are built on ARR multiples, which makes the accuracy of that ARR figure non-negotiable. When a company records the full amount of a prepaid annual contract as revenue immediately, ARR appears higher than it actually is, and this difference is usually identified during investor review. Investors review deferred revenue, revenue recognition policies, and supporting schedules in detail. If the numbers don’t hold up, it can lead to lower valuations or even cause deals to fall through, especially at later stages like Series B[GR4.1] and beyond.

Accurate Internal Decision-Making

Finance teams run the business on recognized revenue, not bookings, not billings, and not cash in the bank. Recognized revenue is what drives budget allocations, hiring decisions, and runway estimates.

If a company assumes it has $2.5M in recognized revenue when the actual figure is $1.8M, it can lead to over hiring and higher spending. Over time, such errors create pressure on cash flow and limit flexibility.

Accurate revenue recognition supports financial planning. It ensures that decisions are based on revenue that has actually been earned, rather than cash that has been collected in advance.

How Revenue Recognition Works in Subscription Businesses

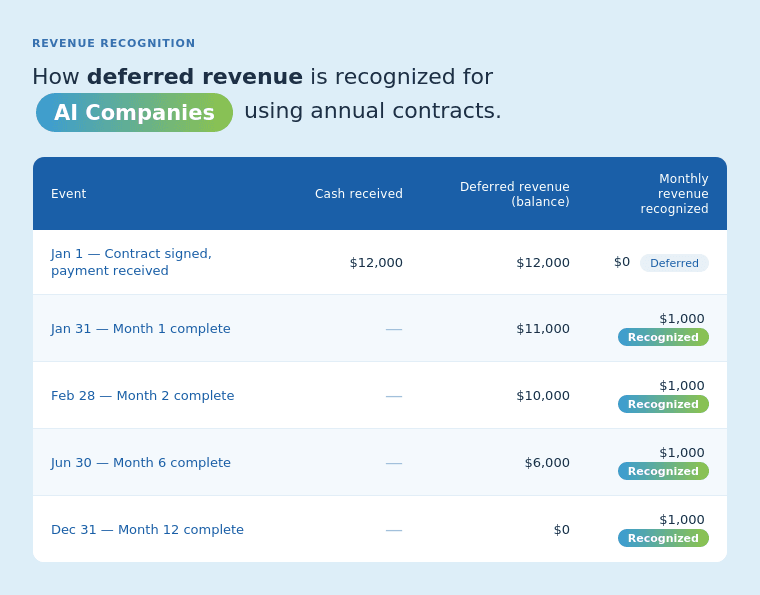

In a subscription model, revenue is earned as the service is delivered, not when the customer pays for it. The gap between cash received and revenue earned is recorded as deferred revenue, a liability on the balance sheet that reduces each period as the company delivers the service.

The simplest version looks like this. A customer signs an annual contract on January 1 and pays $12,000 upfront. That full amount is recorded as deferred revenue on day one. Each month, $1,000 moves from deferred revenue to recognized revenue on the income statement. By December 31, the deferred revenue balance is zero, and the full $12,000 has been earned.

The table above shows a simple case: one customer, a fixed annual plan, and no changes over twelve months. Revenue is recognized in a straight line each month. In practice, SaaS contracts are rarely this clean.

Subscription plans with fixed pricing follow this model, where revenue is recognized evenly across the contract term. If pricing, scope, or contract length changes mid-term, the recognition schedule needs updating from that point forward.

Usage-based pricing doesn't follow this pattern. Revenue is recognized based on actual usage, not a prepaid amount spread over time. If a customer makes 8,500 API calls in January, that usage generates revenue in the same month regardless of what they paid upfront or what the contract says about future months.

Mid-contract changes like upgrades, downgrades, adding seats, or early cancellations make revenue recognition more complex. Under ASC 606, these aren't simple edits to the existing schedule. Depending on the nature of the change, it may be treated as a new contract or as a modification to the current one. Each approach changes how revenue is recognized going forward, and getting it wrong leads to inaccurate reporting and, in some cases, restatements.

These scenarios are covered in detail in the ASC 606 and common challenges sections below. What matters here is simple: recognition accuracy depends on how well contract changes are tracked. As the number of contracts increases and changes build up, it becomes harder to keep track. This is where manual processes fail, and mistakes can lead to restatements.

Key Concepts in SaaS Revenue Recognition

SaaS balance sheets can look confusing until you know what a handful of terms actually mean. These concepts explain where revenue sits at each stage of the billing and delivery cycle.

Deferred Revenue (Contract Liability)

When a customer pays before the service is delivered, that payment cannot be recognized as revenue. It's recorded as deferred revenue on the balance sheet.

Deferred revenue is a liability because the company still owes the customer the service. As the service is delivered for each period, that amount moves from deferred revenue to recognized revenue on the income statement.

Under ASC 606, deferred revenue is referred to as a contract liability. Both terms represent the same obligation, though many companies continue to use “deferred revenue” in their financial statements.

Accrued Revenue (Contract Asset)

Sometimes a company delivers the service before sending the invoice. The revenue is earned, but it hasn't been billed yet. That earned amount sits on the balance sheet as a contract asset until the invoice is issued.

This is common in usage-based models. A customer consumes the service through March, but the billing cycle closes in April. March revenue is already earned. It just hasn't been invoiced, so it lives as a contract asset in the meantime.

It is the opposite of deferred revenue. In deferred revenue, the customer pays first and the service is delivered over time. In this case, the service is delivered first, and payment is collected later.

Under ASC 606, a contract asset represents the company’s right to receive payment. Once the performance obligation is satisfied and the right to payment is unconditional, it becomes receivable.

Recognized Revenue

Recognized revenue is what actually appears on the income statement. It represents the portion of revenue that has been earned by delivering the service.

In fixed subscription models, revenue is recognized evenly across the contract term. In usage-based models, revenue is recognized as the service is consumed.

Recognized revenue reflects what the company has actually earned during a given period and forms the basis for SaaS metrics such as MRR and ARR. Getting it wrong can lead to misleading financial reporting and decision-making, which can ultimately affect investor trust and the company's market valuation.

Why the Terminology Matters

ASC 606 introduced terms such as "contract liability" and "contract asset" to better reflect how revenue is earned and obligations are fulfilled.

Earlier terms such as deferred and accrued revenue focused mainly on cash timing. Contract liability and contract assets focus on performance obligations, showing what the company has delivered and what it still needs to deliver.

During due diligence and audits, investors and auditors go straight to contract asset and liability balances. They want to see how those balances move and why. A company that can't explain the movement clearly creates doubt about its financial health and transparency, and doubt slows down deals

ASC 606 Explained for SaaS

ASC 606 is the accounting standard that governs how companies recognize revenue from contracts with customers. It applies to all US companies following GAAP, public and private, and aligns with IFRS 15, its international counterpart. Both standards share the same underlying framework.

The standard doesn’t specify when companies should collect payments. It tells them when payment becomes revenue. The distinction drives nearly every financial reporting decision made by finance teams in SaaS businesses, where customers often pay months or years before the service is fully delivered.

ASC 606 structures every customer contract into five steps that determine what to recognize and when.

The 5-Step Revenue Recognition Model

Step 1: Identify the contract

A contract exists when both parties have agreed to it, the rights and payment terms are clearly defined, and collection is probable. For most SaaS companies, this is the moment a customer signs a subscription agreement or accepts the terms of service.

Companies often encounter difficulties when it comes to modifying contracts. When a customer upgrades, adds seats, or cancels early, the company must determine whether the change creates a new contract or modifies the existing one.

ASC 606 clearly states that adding a distinct new service at its normal standalone price is treated as a new contract. Changing the scope or price of an existing service modifies the current contract. Each treatment produces a different recognition outcome, and one leads to errors at every subsequent step.

Step 2: Identify the performance obligations

A performance obligation is a distinct promise to deliver a good or service. The test for "distinct" is straightforward: can the customer benefit from it independently without the other elements in the contract?

A standard SaaS subscription is usually one performance obligation, continuous access to the platform, with revenue recognized evenly over the contract term.

Things become more complex when the contract includes multiple elements. Common examples include

- Bundled subscriptions and professional services: Platform access recognized monthly over the contract term.

- Onboarding or implementation: Recognized when the work is delivered.

Each follows its own recognition schedule and can’t share the same timeline.

Step 3: Determine the Transaction Price

The transaction price is the amount the company expects to receive in exchange for delivering the service. For fixed-price subscriptions, the calculation is straightforward. For contracts with variable elements, it requires estimation.

Common sources of variability include

- Usage-based fees

- Performance bonuses or penalties

- Refund clauses and credit provisions

- Tiered or consumption-based pricing

ASC 606 requires companies to estimate these amounts upfront, but with a guardrail. Revenue should only be recognized when the company is reasonably confident the amount will not need to be reversed later. If the final amount is uncertain, the estimate should be conservative rather than aggressive.

A company estimating $50,000 in usage fees without sufficient history cannot recognize the full amount immediately. Doing so and reversing it later is precisely the kind of restatement that damages investor confidence.

Step 4: Allocate the Transaction Price

When a contract includes multiple performance obligations, the total contract price must be allocated based on the standalone selling price (SSP) of each element. The allocation is proportional; each element receives a share of the total contract price equal to its SSP as a percentage of the combined SSPs.

Say a customer pays $25,000 for a bundled SaaS license and implementation project. Individually, these would cost $20,000 and $8,000 for a combined SSP of $28,000. The $25,000 contract price is allocated proportionally:

- License: $20,000 ÷ $28,000 × $25,000 = $17,860

- Implementation: $8,000 ÷ $28,000 × $25,000 = $7,140

Revenue for each element is then recognized on its schedule. Treating both as a single straight-line figure would misstate revenue in every period.

In many SaaS cases, individual prices aren’t clearly defined. ASC 606 allows you to estimate them using three methods.

- Adjusted market assessment: What would a customer in this market pay for this product or service on its own?

- Expected cost plus margin: Estimate the cost to deliver it, then add a reasonable margin.

- Residual approach: Take the total contract price, subtract the known standalone prices of everything else, and what's left is the estimate. This method is only permitted when the standalone price is truly unobservable, not because calculating it is inconvenient or difficult.

Step 5: Recognize Revenue as Obligations are Satisfied

Revenue is recognized when or as the performance obligation is satisfied. This distinction matters under ASC 606:

- As (over time): The customer receives and consumes the benefit continuously. SaaS subscriptions almost always fall here. A twelve-month contract is recognized as an equal amount each month over the entire duration.

- When (point): Control transfers at a specific moment. A one-time data migration or implementation project is recognized at completion, when the deliverable is handed over.

This classification determines whether revenue is spread across multiple periods or recognized in a single period. Moreover, it's one of the most frequently misapplied judgments in SaaS accounting.

Common Revenue Recognition Challenges in SaaS

Revenue recognition gets complicated fast in SaaS. Fixed pricing, usage-based billing, multi-year contracts, and mid-term plan changes all affect how revenue should be recorded.

These are the challenges finance teams run into most often, and where recognition errors are most likely to go undetected until an audit or due diligence process surfaces them.

Multi-Year Contracts with Non-Linear Payments

Most annual SaaS subscriptions are simple: the customer pays upfront and receives service over twelve months. Multi-year contracts with uneven payment schedules require closer evaluation.

Take a three-year contract where year one is free and years two and three are billed at $24,000 each. The customer receives the service before paying for it. ASC 606 requires companies to determine whether that gap creates a financing arrangement. If it does, part of the payment gets recorded as interest income rather than subscription revenue, meaning recognized revenue will come in lower than cash collected. Missing this assessment can overstate revenue and misclassify the financing component entirely.

That said, ASC 606 does offer relief for standard subscription arrangements. Under the one-year practical expedient in ASC 606-10-32-18, companies can skip the financing assessment when the gap between service delivery and payment is one year or less. Multi-year contracts with deferred or back-loaded payment structures fall outside this exception.

Usage-Based and Hybrid Pricing

Many SaaS contracts pair a fixed subscription fee with variable charges such as API usage, storage, active users, and similar metrics. Under ASC 606, each component follows a different recognition approach.

The fixed subscription portion is typically recognized evenly across the contract term. Variable charges are more involved because companies must estimate expected usage, apply constraints, and revisit those estimates as actual usage comes in.

ASC 606 does provide a practical shortcut for pure usage-based pricing. When the invoice amount directly reflects value delivered during that period, companies can recognize revenue at the invoiced amount without running separate estimates.

Hybrid contracts add another layer because they combine fixed and variable elements within the same agreement. A company might estimate $80,000 in usage fees on a new contract with thin historical data, then later find actual usage landed at $51,000. That's a $29,000 revenue reversal, exactly the kind of adjustment that draws attention in audits or investor reviews.

To reduce this risk, finance teams typically estimate variable revenue conservatively and refine those estimates as more reliable usage data becomes available.

Mid-Term Upgrades and Downgrades

When customers upgrade or downgrade plans during a contract, the billing update is usually straightforward. The accounting impact is more complicated.

A mid-contract plan change affects deferred revenue balances, monthly revenue schedules, and sometimes requires adjustments under ASC 606. Many billing systems update the billing correctly to adjust the underlying revenue recognition schedule accurately. Over time, those inconsistencies become harder to track and easier to go unnoticed.

Refunds, Credits, and Service-Level Credits

Refund obligations reduce the transaction price and must be estimated upfront rather than recorded only when a refund occurs. Waiting until a customer asks means revenue has already been overstated in prior periods.

Service-level agreement (SLA) credits also reduce revenue in most cases because they represent variable consideration. However, if the credit provides discounted future services beyond standard contract terms, ASC 606 may treat it as a separate performance obligation. Applying the wrong treatment can affect both revenue recognition and performance obligation accounting, the most scrutinized areas in a SaaS audit.

Bundled Arrangements and Implementation Services

Enterprise SaaS contracts often combine subscriptions with implementation, training, or managed services. Under ASC 606, each element must be assessed as a distinct performance obligation with its own price allocation and recognition schedule.

The key question is whether the customer can use the software without implementation. If yes, implementation is recognized as the work is delivered. If the software genuinely can't function without it, the two may be treated as a single combined obligation with all revenue deferred until go-live. On a $200,000 contract, the difference between these two treatments can shift millions in recognized revenue across a single quarter. It's one of the first things a technical auditor will examine.

Applying revenue recognition to complex SaaS contracts becomes difficult as pricing models, contract modifications, and usage-based billing grow more complex. Manual tracking often leads to recognition errors, reversals, and audit issues.

That’s the problem modern subscription management systems are built to solve. They automate contract changes, revenue schedules, and audit trails, where the operational side of revenue recognition begins.

How Subscription Billing Impacts Revenue Recognition

Billing and revenue recognition are connected, but not the same thing. Billing is when an invoice goes out. Revenue recognition is when the payment is recorded as earned revenue. These two happen at different times, and in SaaS, that gap is often significant. It’s what creates the deferred revenue and accrued revenue balances recorded on every SaaS company's balance sheet.

When a customer upgrades on day 15 of a 30-day billing period, the billing system calculates the prorated charge and issues an updated invoice. At the same time, the revenue recognition system must determine how much revenue was earned before the upgrade, what happens to the remaining deferred revenue balance, and what the new recognition schedule looks like from that point forward. If the two systems aren’t connected, the financial records will become inaccurate, and the finance team[GR1.1]s end up manually fixing records that should update automatically.

Disconnected systems create reconciliation burdens and increase error risk. As contract volume grows, so does the number of upgrades, usage-based adjustments, and mid-term modifications. The manual workload compounds faster than most finance teams can manage. This is why billing and revenue recognition need to operate from the same data source, and not two systems that are periodically synced and hoped to agree.

Automating Revenue Recognition with Software

Managing revenue recognition manually works at low volume. As contracts diversify and modifications increase, spreadsheets lead to errors that compound over time. Automated revenue recognition software reduces this risk by applying ASC 606 and IFRS 15 rules automatically at the contract level. It generates recognition schedules, allocates transaction prices, and posts journal entries to the general ledger without manual work. The result is a recognition process that stays accurate as the business scales without adding headcount to maintain it.

What it needs to do well

- Schedule generation. Creates recognition schedules at contract inception using the correct method: straight-line, usage-based, or milestone-based, depending on the pricing model.

- Modification handling. Recalculates recognition schedules and adjusts deferred revenue balances automatically when customers upgrade, downgrade, or cancel mid-term.

- Multi-element allocation. Allocates transaction price across performance obligations using pre-configured SSP rules; no manual calculation per deal.

- Audit trail. Logs every recognition event with full contract data, traceable from contract inception to journal entry.

- GL integration. Pushes entries directly to NetSuite, QuickBooks, Xero, or Sage; no manual data entry or reconciliation step.

- Real-time reporting. Delivers live deferred revenue balances, waterfall schedules, and performance obligations remaining by customer and period.

The best revenue recognition software for SaaS is not a standalone tool added on top of a separate billing platform. Billing and recognition need to share the same data model. When a customer upgrades, the platform should automatically update the invoice, adjust deferred revenue, generate the new recognition schedule, and post the journal entry all at once. Platforms that push billing data into a separate recognition tool don't solve the problem. They just move it further downstream.

Automate all the revenue recognition process along with billing here

IFRS Reporting Standards for Revenue Recognition

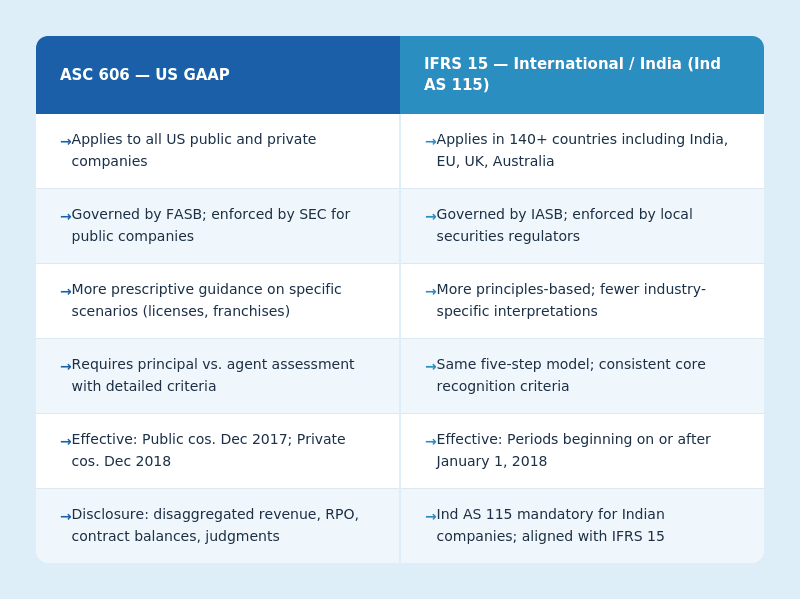

IFRS 15, Revenue from contracts with customers, is the international counterpart of ASC 606, developed jointly by the IASB and FASB to establish a globally aligned revenue recognition framework. SaaS firms raising global capital or listing on foreign exchanges; compliance goes beyond US GAAP and requires alignment with IFRS 15.

Both standards, ASC 606 and IFRS 15, are closely aligned. Both apply the same five-step model covered earlier on this page, and the core principle is identical: recognize revenue when performance obligations are satisfied, not when cash is received.

Where the differences show up in practice

For a company already compliant with ASC 606, the additional IFRS 15 requirements are specific rather than structural:

- Performance obligation guidance: ASC 606 provides more detailed guidance on identifying distinct performance obligations than IFRS 15. In complex cases like bundled contracts, usage-based pricing, and IP licensing, the same contract may be recognized differently under the two standards. Companies that report under both standards should review each case separately instead of assuming the ASC 606 approach will also apply under IFRS 15.

- Setup Fees: Upfront implementation fees that don’t transfer to a distinct service cannot be recognized immediately under either standard. Under IFRS 15, these fees are allocated evenly over the contract term, consistent with ASC 606 standard.

- Contact Acquisition Costs: IFRS 15 requires businesses to capitalize and pay off contract costs, such as sales commissions, over the estimated customer relationship period. This mirrors ASC 340-40 under US GAAP. Companies switching from IFRS to dual reporting often find this the most significant adjustment.

- Financing Components: Multi-year contracts with deferred or upfront payment structures require an assessment of whether a significant financing component exists under both standards. Like ASC 606, IFRS 15 also includes a one-year practical expedient for these assessments.

- Transition method differences: ASC 606 offers slightly more transition flexibility than IFRS 15 at adoption. The modified retrospective approach is the most used method, but the practical simplifications available are different from those under ASC 606

Keeping contract asset and liability balances aligned across both frameworks matter most when international investors are involved. Revenue recognition that complies with both standards is one of the first things an international buyer or VC will review during due diligence.

ASC 606 vs IFRS 15 - Key Differences for SaaS Companies to know.

Best Practices for SaaS Revenue Recognition

Getting revenue recognition right in SaaS isn't a one-time compliance process. As contracts change, pricing models evolve, and transaction volume grows, maintaining accuracy becomes increasingly challenging.

The practices below build the foundation that holds up as the business scales.

Document Contracts and Modifications at Inception

Revenue recognition compliance starts with documentation. Every contract, amendment, and modification should be recorded when it happens, & not reconstructed later from emails and invoices.

These records form the foundation for every subsequent revenue recognition decision. When an auditor asks why a deferred revenue balance changed, the answer should be clearly documented and easy to trace. A complete contract record from the start makes SSP allocation, contract modification handling, and audit reviews far easier to manage.

Establish Documented Standalone Selling Prices

Accurate revenue allocation under ASC 606 and IFRS 15 depends on clearly defined standalone selling prices for every product and service. Without documented SSPs, finance teams often rely on estimates, which can lead to inconsistent revenue allocations.

These inconsistencies become difficult to justify during audits. To keep allocations accurate, SSPs should be reviewed regularly and updated whenever pricing changes or new products are introduced.

Align Sales, Legal, and Finance Before Contracts Are Signed

Revenue recognition problems rarely start in the finance team. They start in the sales process with a non-standard payment term, a custom discount, or a bundled arrangement that creates accounting complexity later.

Sales and legal teams need to understand how certain contract terms can affect revenue recognition. Finance teams need visibility before contracts are executed, not after. This alignment prevents the most common recognition errors from entering the system in the first place.

Review Recognition Schedules Regularly

Revenue recognition schedules should be reviewed regularly & not just during the annual audit. Small errors in allocations or deferred revenue balances can grow into larger issues if they go unnoticed. These problems usually surface at the worst possible moment, during a fundraise, an acquisition review, or under year-end scrutiny.

Monthly reviews give finance teams a chance to catch and resolve issues before they reach the financial statements. They also make audits faster and reduce the need for last-minute adjustments.

Treat Renewals as Accounting Events, Not Administrative Ones

Most SaaS finance teams process renewals as routine billing events. However, under ASC 606, they aren't. A renewal that includes modified pricing, changed contract terms, or newly bundled services triggers the same modification assessment as a mid-term plan change. The question is always the same: does the renewal create a new contract or amend the existing one?

A renewal processed without that assessment can carry existing revenue recognition errors into the new contract term. This can result in ongoing errors in revenue schedules and financial reporting. To avoid this, finance teams should review renewals for contract changes and update revenue recognition schedules whenever those changes affect how revenue is recognized.

Invest in an Integrated Tech Stack

As contract volume grows, the disconnected systems become the main source of recognition errors. Billing platforms, revenue recognition tools, and accounting systems need to be working from the same contract data. When these are connected, a mid-contract upgrade automatically updates deferred revenue balances, recognition schedules, and general ledger entries without manual intervention. When they operate separately, finance teams must manually reconcile differences at month-end.

These issues increase as the business handles more contract changes, renewals, and new pricing models. The right tech stack doesn't just reduce manual work; it makes the recognition process auditable and scalable without needing to add headcount to keep up.

Key Revenue Recognition Metrics to Track

Most SaaS finance teams closely track MRR and ARR. But those numbers don't tell you whether revenue is being recognized correctly. For that, teams need to see deferred revenue, unbilled revenue, and recognition schedules. This is because that's where billing gaps, timing errors, and recognition problems actually show up.

Miss any of these, and it shows financial reports, audit findings, investor reviews, and forecasts that don't hold up under scrutiny.

Deferred Revenue Balance

Deferred revenue is cash collected for services not yet delivered. It appears as a liability on the balance sheet until the service is delivered and the revenue is earned.

Finance teams should monitor deferred revenue balances to understand future revenue and ensure recognition schedules remain accurate. A decline in deferred revenue that doesn't align with the revenue recognition schedule may indicate errors, contract cancellation, or modification that were not properly reflected in the schedule.

The Revenue Waterfall

The revenue waterfall is a period-by-period schedule that shows when deferred revenue converts into recognized revenue across upcoming months and quarters. It answers a question that ARR alone cannot: if the sales pipeline slowed down today, how many months of revenue are already secured through existing contracts?

For fundraising or investor review, the revenue waterfall is the first report they ask

When a SaaS company raises funding or prepares for an acquisition, investors and buyers often ask to review the revenue waterfall report early in the process. It gives insight into how well the company manages its revenue recognition process.

A clean revenue waterfall tied directly to contract data signals that recognition is under control. One that can't be reconciled to the balance sheet is usually a sign that something in the recognition process has gone sideways.

Unbilled Revenue (Accrued Revenue)

Unbilled revenue is the opposite of deferred revenue. The service has been delivered, but the invoice hasn't gone out yet. It appears on the balance sheet as a contract asset until billing occurs, most commonly in usage-based and hybrid models.

Tracking the unbilled revenue balance helps finance teams understand the gap between service delivery and billing. An increasing unbilled revenue balance should be analyzed carefully. Is usage accelerating? Are billing cycles misaligned with usage? Are invoices delayed? Each scenario carries different cash flow implications and needs to be understood on its own terms.

MRR vs. Recognized Revenue Variance

MRR and recognized revenue measure different aspects of SaaS revenue, and the gap between them provides useful information about the company’s revenue patterns.

MRR measures predictable monthly subscription revenue. Recognized revenue reflects what was actually earned in a period under ASC 606 after accounting for contract modifications, variable consideration, and multi-element allocation.

Three factors commonly cause a difference between MRR and recognized revenue. They are:

- Different month durations

Recognition may vary based on the number of service days in a month, while MRR remains fixed as a monthly metric.

- One-time fees

Implementation, setup, or other non-recurring charges may be recognized as revenue but are not included in MRR.

- Usage charges and mid-cycle changes

Overages, fees, upgrades, downgrades, and other contract changes can affect recognized revenue in ways that MRR doesn't capture.

When MRR grows faster than recognized revenue, it often indicates an increase in deferred revenue that will be recognized in future periods. When recognized revenue exceeds MRR, the company may be recognizing revenue from one-time fees, usage-based charges, or contract adjustments that are not reflected in MRR.

Deferred Revenue Movement (Rollforward)

The deferred revenue rollforward tracks how the balance moves from one period to the next.

It shows,

- How much new deferred revenue was added from new contracts and renewals.

- How much was converted to recognized revenue as obligations were satisfied.

- How much was removed due to cancellations, refunds, or contract modifications.

A deferred revenue balance can stay flat while significant activity flows through it; new contracts get added to the balance while existing ones burn down. The rollforward makes that activity visible.

Auditors review it directly. Investors use it to project future recognized revenue. A clean rollforward supported by contract-level data provides a clear audit trail for changes in deferred revenue.

What These Metrics Have in Common

None of these metrics is useful if the underlying data isn't accurate. Deferred revenue balances should tie back to contract records. Revenue waterfall schedules should reconcile to the balance sheet. When they don't, it often points to revenue recognition issues. In most cases, the underlying problem is incomplete or inaccurate contract-level tracking.

That's why the metrics in this section are both reporting outputs and early warning indicators. They don't just show what happened. Instead, they show where the recognition process is working and where it isn't.