Most revenue recognition errors don't start with bad accounting. They start when there's a delay between service delivery and billing. Accrued revenue is what fills the gap and it ensures that the earned revenue is recorded in the correct accounting period.

What is accrued revenue?

Accrued revenue is the income a business has earned by delivering products or services but hasn't yet been invoiced or collected from the customer. This means the work is done. But the payment just hasn't moved yet.

Accrued revenue occurs when there is a delay between delivering a product or service and billing the customer. The transaction is accounted for whenever the performance obligation is met, regardless of whether an invoice has gone out or payment has come in.

This practice is especially common in SaaS;

- Quarterly or annual billing cycles

A customer is billed every quarter, but the service is delivered month by month. The months between billing dates generate accrued revenue.

- Mid cycle subscription changes

A customer upgrades seats or adds a feature partway through a billing period. The platform delivers the upgraded service immediately, but the charge appears in the next invoice.

- Usage-based pricing

Consumption happens in real time, but measurement and billing happen at the end of the period.

- Professional services

Implementation, onboarding, migration, or training is delivered before the invoice is issued.

In each case, the obligation has been fulfilled. Billing just hasn't happened yet.

Accrued Revenue Under ASC 606 and IFRS 15

ASC 606 (US GAAP) and IFRS 15 require companies to recognize revenue when they satisfy a performance obligation, not when they issue an invoice or collect payment.

A SaaS company recognizes revenue as soon as it delivers the promised service, even if the customer has not yet been billed. Until the invoice is issued, the company records the earned amount as a contract asset on the balance sheet. When the invoice is issued, the contract asset is reclassified as accounts receivable.

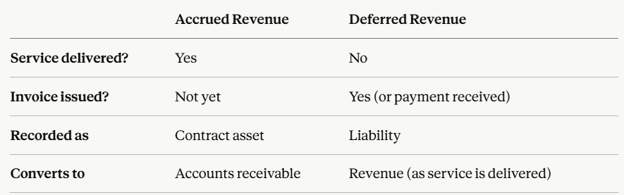

The Difference: Accounts receivable represents billed but unpaid invoices. A contract asset represents earned revenue for products or services that have been delivered but not yet invoiced.

Accrued Revenue vs. Deferred Revenue

Although accrued revenue and deferred revenue are often confused, they represent opposite stages of the revenue cycle.

Accrued revenue is earned but not yet invoiced or collected.

Deferred revenue is the amount that is billed or collected in advance for goods or services that have not yet been delivered.

Accrued Revenue Example in SaaS

A marketing agency subscribes to a SaaS platform on a quarterly billing plan. Halfway through the billing cycle they add ten user licenses and request a custom training session. The platform delivers both services right away, but the charges won't appear until the next invoice.

For that period, the platform records the value of the licenses and onboarding sessions as a contract asset. When the quarter ends and the invoice goes out, the amount converts to accounts receivable. Once the agency pays, it is recognized as revenue.

Why It Matters for SaaS Finance

Subscription businesses often deliver services before customers are billed. If that earned revenue isn't recorded, financial statements may not accurately reflect the company's financial performance. Tracking accrued revenue ensures revenue is recognized in the correct accounting period rather than when invoices are issued.

For SaaS businesses it also supports;

- Accurate MRR and ARR reporting.

- Better investor and board reporting.

- More reliable cash flow forecasting.

- Accurate profitability by accounting period.

- Audit readiness and ASC 606 compliance.

Want to know more about elevating your subscription Billing and Revenue Recognition? saaslogic provides the solutions you need.

Connect with our experts today!

REQUEST DEMO